U.S. Gross Transportation Tax - Recouping Down the Chain

Steamship Mutual

Published: December 01, 2012

In three arbitration appeals, the Commercial Court were asked to address which party or parties in a string of charters had to bear the cost of US Gross Transportation Tax (“USGTT”).

The time charters in the chain were on an amended NYPE form with materially identical terms and included the BIMCO US Tax Reform 1986 clause (as recommended by the BIMCO circular No.9 of 6 July 1988)

The clause reads as follows:

“Any U.S. Gross Transportation Tax as enacted by the United States Public Law 99 – 514, (also referred to as the U.S. Tax Reform Act 1986), including later changes or amendments, levied on income attributable to transportation under this Charter party which begins or ends in the United States and which income under the laws of the United States is treated as U.S. Source Transportation Gross Income, shall be reimbursed by the Charterers.”

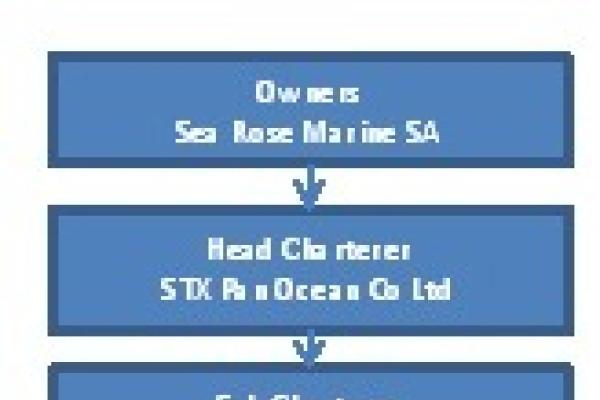

The charter chain was as follows:

Sangamon had ordered the vessel to call at US ports and as a result, as the vessel’s owners, Sea Rose incurred liabilities of US$ 134, 400 in respect of USGTT. Head Charterers, STX Pan Ocean reimbursed this amount to owners and sought to pass the liability to their immediate sub-charterer, Global Maritime. Global Maritime in turn sought to pass the liability down the chain to Navios, whom then attempted to pass the liability to Sangamon. All three sub-charterers contested their liability and three arbitrations followed.

In the arbitration between STX Pan Ocean and Global Maritime, the tribunal found that the charterer was accountable to the disponent owner for USGTT. Contrast this with the arbitrations between sub-charterers (in which there was only one common arbitrator with the head arbitration), Global Maritime/Navios and Navios/Sangamon, where the tribunal found by a majority that charterers were not entitled to reimbursement from their sub-charterer.

This left Global Maritime in the unfortunate position whereby they were bound to reimburse STX Pan Ocean but unable to claim reimbursement from Navios. The unsuccessful parties appealed to the Commercial Court. All parties agreed that Pan Ocean would advance the case on one side and Sangamon the opposing case.

The substantive issues for the Court to consider were as follows:

i. the relevance of the BIMCO circular on the question of construction; and

ii. the meaning and effect of the BIMCO US TAX Reform 1986 clause.

Mr Justice Clarke held that Sea Rose as the shipowner was entitled to a reimbursement from the head charterer, STX Pan Ocean in respect of the USGTT it had paid, but no one else in the chain was entitled to reimbursement. In construing the meaning of the clause, the tribunals were entitled to take into account the Circular as part of the relevant background. It was reasonably available to any party in a charter and a party can be expected to know what is reasonably available to them. The Circular was valid as evidence as it set out the risk with which the clause was designed to deal.

He considered that the words in the clause “levied on income attributable to transportation under this Charter party” when read in the context of the sub-charters were not apt to cover tax levied on income received under the head charter. The clause as it stood, dealt with tax levied on hire due under the charterparty between owners and head charterers. Furthermore, ‘tax’ and ‘reimbursement in respect of tax’ were different things and the court could find no sufficient reason to construe “any….tax” to cover reimbursement for tax.

The court observed that the circular highlighted that each charterer in the chain might, as disponent owner, be liable for the tax and that the clause provided for such owner to recover the tax it has paid from its charterer. It did not say anything about liability for one or more taxes cascading down the chain to the end charterers.

In light of this decision, where it is contemplated that a vessel may call at US Ports, parties should consider amending the BIMCO clause or include another provision to indemnify them in relation to any liability to US tax. Inclusion of the BIMCO US Tax Reform 1986 will not entitle disponent owners to reimbursement from sub-charterers.

On a side note, the inconsistent decisions at the arbitration stage highlight the need for concurrency when dealing with arbitrations arising out of a charterparty chain. The use of one tribunal for all three arbitrations may have avoided the inconsistent decisions.

If you have any questions and/or concerns, please seek advice from the Club in the usual manner.

Global Maritime Investments Ltd v STX Pan Ocean Co Ltd: Global Maritime Investments Ltd v Navios International Inc: Navios International Inc v Sangamon Transportation Group [2012] Ewhc 2339 (Comm)

Article by Nathaniel Harding